【1】Intro to Microeconomics

⭐Economics - study how we use scarce resources to best satisfy our unlimited material wants

Microeconomics - individual industries/business firms/households' decision making and behavior

Macroeconomics - examines the economic behavior of aggregates (income, output, employment, etc. on a national scale)

Opportunity cost - tradeoff (something we give up) in order to make a decision because time and resources aren't unlimited; value of what's given up during a tradeoff

Marginalism - in weighing both pros and cons of a decision, it's important to weigh both costs and benefits that come from making it.

- Ex. when deciding whether to produce additional output, firms consider marginal, not sunk cost (costs that are unavoidable, regardless of what happens in the future)

Efficient markets - profit opportunities are taken up almost instantaneously; increase in job market & ready supply of workers

Methods

Normative economics - policy economics; good & bad outcomes; comes up with course of action

Positive economics - studies and describes economic behavior without making judgements; describes how it works and exists

- descriptive economics - collecting data in order to describe its facts and phenomena

- economic theory - building models of behavior

Empirical economics - using data to test economic theories

Theories and Models

Occam's razor - cuts irrelevant details because models should be a simplification of reality

ceteris paribus - "all else equal"; studying relationship between 2 variables while having other variables unchanged

Pitfalls in creating theories and models

Post Hoc Fallacy - misconception that just because event A happened before event B, event A caused event B

Fallacy of Composition

Criteria of judging economic outcomes

- Efficiency - produces what people want for as little cost as possible

- Equity - fairness of economic outcomes

- Growth - increase in total output of an economy

- Stability - output is steady or growing; low inflation and full employment of resources

Scarcity - limited resources, unlimited wants

Resources - factors of production

- Labor - human effort and talent, mental and manual

- Land - gas reserves, farmland, oil, water, mineral deposits

- Capital - investment

- physical - machines, roads, buildings, vehicles, tools, etc.

- human - knowledge from experience and education

- Entrepreneurial ability - putting resources together in a productive venture; planning

5 Key Economic Concepts

- Scarcity

- Choices have a cost (trade-off)

- Everyone's goal is to make choices that maximizes their satisfaction (acting on self interest)

- Everyone makes decisions by weighing marginal costs and marginal benefits

- Models/graphs can explain and analyze real life situations

Trade-offs - all alternatives that we give up whenever we chose 1 action over the others

|

Example: "15 minutes could save you 15% or more on your car insurance" |

- Individual trade-offs: renting/buying/leasing a house, transportation, grocery store items, employment opportunities

- Firms: which goods/services, how much should be produced, how to produce, how much should employees get paid

- Government: large decisions, both local and national; immediate or long term consequences

Cost-Benefit Analysis - making decisions by weighing the costs v. benefits of an action

- total costs > benefits = no action

- total costs <= benefits = maybe/will act

total cost - value of all things given up to do something (explicit costs + implicit costs)

- explicit costs - upfront, direct out of pocket expenses from decision

- implicit costs - value of next best thing you could've done

total benefits - depends on the evaluation of the person making the decisions

- "How much would I pay at most for x"

- Willingness to pay - max price of total benefit

Marginal Analysis - making decisions based on costs and benefits of doing/consuming the next one

- the consumer weighs the additional cost and benefits

marginal cost - addition cost from consuming the next unit of a good or service

marginal benefit - additional benefit received from the consumption

- MB >= MC = do it

- MB = MC = stop

- MB < MC = don't do it

Resource Allocation and Economic Systems

3 Economic Questions (3EQs)

- What goods/services should be produced?

- How should they be produced?

- Who are the consumers?

Centrally-planned Economics (Communism)

- Government owns all resources and answers all 3EQs

- No incentive for working hard because most of the time, the government is corrupt

- No profit/way to get ahead

- poor goods, shortages, and unhappy citizens

- Irrational Soviet Production - Soviet companies were not guided by prices or profit. The government determines output quotas on quantitative measurements. Businesses were paid based on meeting those quotas

- Pros

- Low unemployment

- Good job security (the government doesn't just simply "go out of business")

- Equalized income

- Free healthcare

- Cons

- No innovation

- Zero competition; goods' quality = poor

- Corrupt leaders

- Few individual freedoms

Free Market Economics (Capitalism)

- Operates on Laissez Faire - little government involvement

- Individuals own goods and answers the 3EQs

- opportunity for profit = incentive to produce quality items more efficiently

- Provides a variety of goods for consumers

- Competition + self-interest = prices decrease, quality increases

- "Invisible Hand"

- Societies' goals will be met as people seek their self-interest

- Society wants X, profit-seeking producers will make more of X

- Competition between firms = lowered prices, increase in quality and efficiency

- Government doesn't get involved because needs are being met automatically

- Cons

- Companies are greedy; takes advantage of the average population

- They outsource jobs overseas

- Only help the rich

- Sweatshops

- "have voluntary workers overseas because it's better than the alternative (working in certain other jobs)"

Broad Social Goals

- Economic Freedom

- Economic Efficiency

- Economic Equity

- Economic Security

- Full Employment

- Pull Stability

- Economic Growth

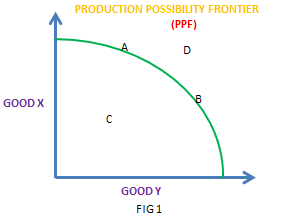

Production Possibility Graphs

When deciding how to spend scarce resources between 2 goods/services, economists uses

models

- Assumptions

- only 2 goods can be produced

- full employment of resources

- fixed resources (ceteris peribus)

- fixed technology

Production Possibility Frontier - line of the curve (outer limits of production)

- above the curve = unobtainable with current resources

- below = inefficient use of resources

- on = efficient

Productive Efficiency - things are produced in the least costly way; any point on the PP curve

Allocative Efficiency - things being made are desired by society; the optimal point on PP curve depends on desires of a society

Resource Sustainability

- when changing the goods we produce, our resources must be moved into that industry

- the new industry may be better/worse at production, it's rare for 2 things that have the exact same production costs

- Constant opportunity cost - when resources are easily adaptable for producing either of the 2 goods on the PP graph (straight PP curve)

- Law of Increasing Costs - the more of a good is made, the greater the opportunity cost; creates a concave PP curve (bowed out)

marginal unit costs: Opportunity Costs/units gained

3 Shifters of PP Curve

- resource quantity/quality

- technology

- trade

Services - actions/activities a person performs for another

Goods - physical things that satisfies wants or needs

Consumer good - something you buy and use once; direct consumption

Capital good - an investment; used to make other goods and services; indirect consumption

Capital Goods & Future Growth

- Countries that produce more capital/business goods will have greater growth than those that focus on capital goods.

Utility - Satisfaction

Marginal - Additional

Shortage - when producers can't or won't offer goods/services at current prices because they can't keep up with current demand at their current price

Price - amount the consumer pays

Cost - amount the seller pays to produce a good

Investment - using money for something for a financial return for the future

Specializing in the production of a good/service promotes trade

Limiting trade reduces people's choices and makes living worse

More access to trade = more chances at a higher standard of living

⭐ Countries should trade if they have the lower opportunity cost for the things they're producing so it's beneficial for them if they specialize in the good that's "cheaper" for them to make.

Per Unit Opportunity Cost = opportunity cost/units gained

Absolute advantage - producer that makes more given the same amount of resources

Comparative advantage - the producer who can produce at a lower opportunity cost

⭐Specialization - focusing on one or few products to become more efficient

- Pros

- There's a lower opportunity cost for making the products you want to sell

- Firms make more profit

- Consumers benefit by buying goods at lower prices

Calculating Opportunity Costs

Through output (products produced over a fixed time)

- 1A = B/A of B

Through input (cost of labor in terms of labor and time)

- 1A = A/B of B

For a fair trade, the price should be between the opportunity costs of both countries for that good

Product Market - where consumers go to buy things

Resource/Factor Market - where producers go to buy things (4 types of resources)

utility - happiness/satisfaction

- marginal utility - for an additional amount of good x, how much more utility you gain

- total utility - how much utility you get from a certain amount of good x.

Comments

Post a Comment